Our economy has a problem. In fact, it has a number of problems, but one in particular. Inflation is increasing significantly faster than income for most people. Therefore, even if you’ve gotten a cost of living increase, chances are your paycheck today doesn’t go nearly as far as it did a few years ago. That also means if you’ve been paying the same amount into your IRA/401(k) over that time, that’s not going to go as far either.

Understanding Inflation

When you first started building your nest egg, the amount you were paying in regularly seemed like it would be enough; by the time you reached retirement age, to support you for the remainder of your life. But if you do the same math today, chances are you’ll find yourself coming up short. It’s the same amount it always was, but that money simply doesn’t go as far anymore.

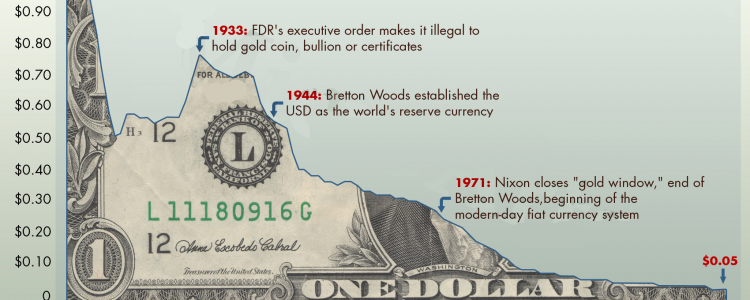

Think of it another way: How much did a candy bar cost when you were a kid? A quarter? Fifty cents? Now that same candy bar costs well over a dollar, and it’s a lot smaller. Everything is more expensive than it used to be—often many times more expensive. Price inflation is a fact of life, and it causes your cash to lose value over time. By the time you reach retirement age, that cash will have devalued even more, and prices will be even higher. What seemed like enough to live on when you started out will end up running out much faster than you anticipated, leaving you struggling in the last years of your life.

Combating Inflation with Gold

In order to maintain the value of your retirement nest egg, you need to invest it in something that’s not subject to inflation; a physical asset that will continue to maintain value, and buying power, over time. Sadly, there are fewer and fewer assets that can do that anymore. Real estate used to appreciate reliably, but after the housing crisis of 2008 it’s a much riskier market than it used to be. Even bonds are losing value over the last few years.

However, there’s one asset remains a reliable investment that’s not subject to inflation: gold. Say you take a $100 bill and $100 worth of gold coins, and put them away for 30 years. After that time, you’ll still have exactly $100 in cash—but it won’t be able to buy nearly as much as it does today. However, the gold will be worth much more than $100. The value of the gold itself hasn’t gone up. But its buying power has remained constant, even in the midst of inflation.

Your retirement savings will need to be able to cover all the same expenses you have now—things like food, clothing, bills, etc.—plus escalating medical care and a variety of additional expenditures. The money you need to spend will be greater, but the cash in your retirement account, even as you add to it over time, will be worth less due to inflation.

However, if you invest your retirement savings in physical gold, then thirty years from now that gold will have the same buying power it does today—if not more. Gold also remains stable as the markets fluctuate, making it more secure than stocks and bonds. With gold in your retirement account, you can add not just money to your IRA/401(k), but actual, lasting value.

Gold Investment is the alternative currency that can safeguard you from these types of events. Putting a portion of your savings into this precious metal will help protect you. Download your free self directed IRA rollover gold IRA information kit today.