The latest consequence of economic mismanagement in Europe was the failed attempt at constitutional reform in Italy this week.

The Italian people have had enough of their government’s economic failure, and is refusing to give it more power.

The EU and the euro project have been an economic disaster for all participants, including Germany, which will eventually be forced to write off the hard-earned savings she has lent to other Eurozone members. We know, with absolute certainty, that the euro will self-destruct and the Eurozone will disintegrate.

We know this for one reason above all. The political class and the ECB are guided by economic beliefs – I cannot dignify them by calling them reasoned theory – which will guarantee this outcome. Furthermore, they insist on using statistics that are incorrect for the stated function, the best example being GDP, which I have criticised endlessly and won’t repeat here. Furthermore, the numbers are misrepresented by government statisticians, CPI and unemployment figures being prime examples.

This article takes a column written by William Hague for the Daily Telegraph published earlier this week to illustrate the depths of misunderstanding even a relatively enlightened politician suffers, with this mix of nonsense and statistical propagandai. This article also refers to a speech delivered this week in Liverpool by Mark Carney, Governor of the Bank of England, showing how out of touch with reality he is as well. Many of his and Lord Hague’s misconceptions are shared by almost everyone, so for the most part go unnoticed.

Lord Hague basically blames the euro for all Europe’s ills: “…… it has made some countries, like Italy and Greece, poorer while others get richer”, he opines, and it is certainly a common sentiment. But it is never the currency that’s to blame, but those that attempt to use it to achieve policy outcomes, and inevitably fail in their quest.

Before the euro came into existence, different currencies offered different interest rates, reflecting the market’s appraisal of lending risk. So, the Greek government, borrowing in drachmas, would typically have to pay over 12% interest, while Germany might pay 3% for the same maturity in marks. The fact that there were differing rates in different currencies imposed market discipline on borrowers.

After the introduction of the euro, interest rates for sovereign borrowers converged towards the lowest rate, which was Germany’s. The reason for this was banks could gear up their lending in the bond and money markets to make easy money from the spread between German rates and the others, risk-free on the assumption that the whole caboodle was guaranteed by the EU and the ECB. It was perfectly reasonable to expect this outcome, but whether the panjandrums in Brussels were smart enough to know this would happen is not clear. If they were, they displayed ignorance of the eventual consequences, and if not, they were simply ignorant, full stop.

These same operatives bent the rules they themselves had originally set to allow countries to join the euro. Under the Maastricht Treaty, budget deficits were to have been less than 3% and government debt to GDP less than 60% for a state to qualify for membership. Neither Germany nor France qualified at the outset. And when it came to Greece, the Greek government simply lied, with the full knowledge and encouragement of the other members. No, Lord Hague, it was the policy makers that were at fault, not the currency itself.

But he continues: “Membership of the euro has put the Italians on a permanent path to being poorer”. Not so. It was the Italians who used cheap euro-denominated money to borrow profligately. They, and they alone are responsible for the mismanagement of their economy and their debt problems, which incidentally now exceed the Maastricht 60% limit by a further 75%.

So, who is policing that?

Lord Hague also trots out the canard about how the euro benefits Germany: “Germans keep exporting easily and running up a surplus, while the Italians struggle and go deeper into debt”. This statement in quotes is undoubtedly true on face value, but it is wrong to blame the poor euro. Instead, the blame lies with fiscal imbalances, relative rates of bank credit expansion, and the additional horror of TARGET2. This last artifice is intended to even out the monetary imbalances that would otherwise occur from trade imbalances. But its designers seem to have been completely unaware that the only way trade imbalances can be controlled is through the money shortages and accumulations that result from trade deficits and surpluses respectively. Instead, TARGET2 makes good the money deficiency that results from excess imports, and reduces the money surplus that accumulates in the hands of the exporters. It recycles the money spent by Italians so that it can be spent again, or even hoarded outside Italy, ad infinitum. TARGET2 is living proof of the ridiculousness behind the euro project.

Lord Hague provides an exception to his argument and conclusion, by citing Germany’s greater productivity and suggesting that the only way out was for Mr Renzi to enact bold reforms to raise Italian productivity to the same level as Germany’s. He doesn’t say what these reforms might be. I can tell him: the new government should downsize from 52% of GDP to less than 40%, the lower the better. The redeployment of capital from government destruction to private sector progression will work wonders. Tax policies should favour savers. At the same time, ordinary Italians should be allowed to get on with their lives and made to understand the state is not there to support them with handouts.

Finally, Lord Hague’s conclusion, while correct legally, is incorrect from a strictly economic point of view. He states that leaving the euro is a far more difficult problem than leaving the EU, there being no Article 50 to trigger. He implies that if Italy simply returns to the lira, there can be little doubt that it will rapidly collapse taking its banks with it, because Italy’s creditors will still expect to be repaid in euros while the cost of borrowing in lira is bound to increase rapidly, undermining government finances.

However, contrary to everything Keynesians have been taught and in turn teach gullible students, the economic objective of monetary independance should be sound money, not continual depreciation. Italy has enough gold to arrange a gold exchange standard for herself, or alternatively she could run a currency board with the euro, to ensure the lira retains value for foreign creditors. Either course requires something novel from Italian politicians: they must bite the bullet on government finances and permit capital to be redeployed from moribund businesses to new dynamic entrepreneurial activities. It can be done, and Italy would rapidly emerge as a new industrial force.

But will it be done? Sadly, there’s not a snowball in hell’s chance, and here we must agree with Lord Hague. In common with their opposite numbers everywhere else, Italian politicians have surrounded themselves with economic yes-men, trained at the expense of the state to justify state interventions in the economy. It has become a feed-back loop that ultimately concludes with economic instability, crisis and eventual collapse.

Carney’s groupthink

Lord Hague, while respected as a senior British politician is at least not involved in Italy’s monetary or fiscal policies. Far more dangerous potentially is someone with his hand on the monetary tiller, Mark Carney, Governor of the Bank of England. This week he made a speech in Liverpool, which put the blame for the failure of his monetary policies on everyone but the Bankii. He said politicians need to foster a globalisation that works for all. Really? How are they going to do that? He blames economists for been at fault for not recognising “the realities of uneven gains from trade and technology”. But surely, we all know that establishment economists, including the Bank’s own, have an unrivalled track record of getting things wrong. To expect them to suddenly exhibit forecasting prescience is Carney’s personal triumph of hope over reality. Carney berates companies for not paying tax. This is the classic “someone else’s fault” line, and ignores the easily proven fact that money deployed by the private sector in pursuit of profit is productive, while giving it to government is wasteful. More tax paid may be desired by the state, but it is anti-productive.

The Governor then claims the Bank’s monetary policy has been “highly effective” and that “the data do not support the idea that the period of low rates has benefited the wealthy at the expense of the least wealthy.” He has obviously been unable to make the connection between the falling purchasing power of fixed salaries for the low paid and for pensioners relying on interest income, while stock markets roar to all-time highs on the back of suppressed interest rates and injections of money through quantitative easing. Yes, Mr Carney, my middle-class friends have done very well out of their investments and property, thanks to monetary inflation, but they still pay their gardeners and maids roughly the same depreciated wages.

This is relevant not only to the mismanagement of the UK’s economy, but also that of Europe. Carney attracted considerable criticism, rightly, for falsely threatening economic hell and damnation in the event of a vote for Brexit. This presupposes that everything in Europe is considerably better than for Britain on its own, and confirms that his opposite numbers in Europe, who were pushing the same line, have as much grasp of the economic situation as he has. Carney got this as wrong as he possibly could, but there’s no mea maxima culpa.

If Mr Carney and Lord Hague want to criticise current economic events, they should start by properly understanding the negative effects of fiscal and monetary intervention. They should realise that propping up defunct enterprises by lowering the cost of borrowing and supporting them with government contracts is Luddite and destructive. And above all, they should realise that ordinary people going about their business are infinitely adaptable, have an ability to withstand government and central bank silliness to a remarkable degree, and would deliver their taxes much more effectively if they were simply allowed to just get on with their business without having to suffer from government and central bank micro-management.

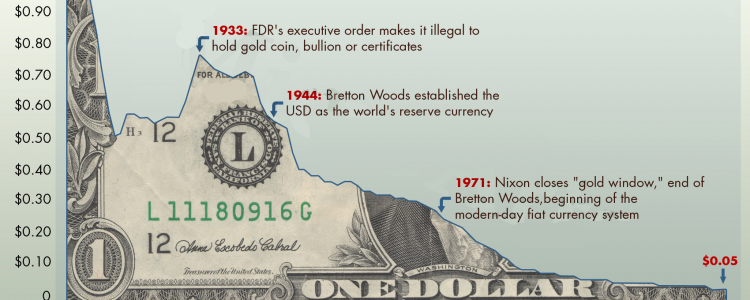

Gold Investment is the alternative currency that can safeguard you from these types of events. Putting a portion of your savings into this precious metal will help protect you. Download your free self directed IRA rollover gold IRA information kit today.